When you fill a prescription for a specialty drug like insulin, rheumatoid arthritis medication, or a cancer treatment, the price tag can be shocking-even if you have insurance. That’s where prescription assistance programs come in. These aren’t charity drives or government handouts. They’re direct support programs run by pharmaceutical companies themselves, designed to help people afford the medications they need. For many, these programs are the only reason they can stay on their treatment.

Two Types of Help: Copay Cards and Free Medications

There are two main kinds of assistance from drug makers: copay assistance programs and Patient Assistance Programs (PAPs). They serve very different groups and work in completely different ways.Copay assistance programs are for people who have insurance but still struggle with out-of-pocket costs. Think of them as coupons you use at the pharmacy. If your copay is $150 for a monthly medication, the manufacturer might cover $120, leaving you to pay just $30. These are usually delivered as physical cards or digital codes you show at the counter. The program pays the pharmacy directly. They’re common for brand-name drugs-especially specialty medications-and about 85% of these high-cost drugs now offer some form of copay help, according to the Kaiser Family Foundation.

Patient Assistance Programs (PAPs), on the other hand, are for people without insurance or with very limited coverage. These programs give you the medication for free-or for a tiny fee-based on your income. You don’t pay a copay. You don’t pay coinsurance. You just get the pills. Some PAPs have been around since the 1980s, originally created during the HIV/AIDS crisis to help people who couldn’t afford life-saving drugs. Today, 92% of major drug manufacturers run at least one PAP. In 2022 alone, these programs gave out $24.5 billion worth of medication to 12.7 million people.

Who Qualifies? Income, Insurance, and Rules

Eligibility isn’t the same for both types of programs.For copay assistance, you usually need to have private insurance. You can’t use these cards if you’re on Medicare Part D, Medicaid, or another government plan. Why? Because federal rules and state laws restrict how these programs can interact with public insurance. Many states, including California and New York, have passed laws limiting or banning copay cards for Medicaid patients. Some insurers even have "copay accumulator" programs that don’t let the manufacturer’s discount count toward your deductible. That means even if you’re using a copay card, you’re still paying full price toward your deductible-just not out of your own pocket.

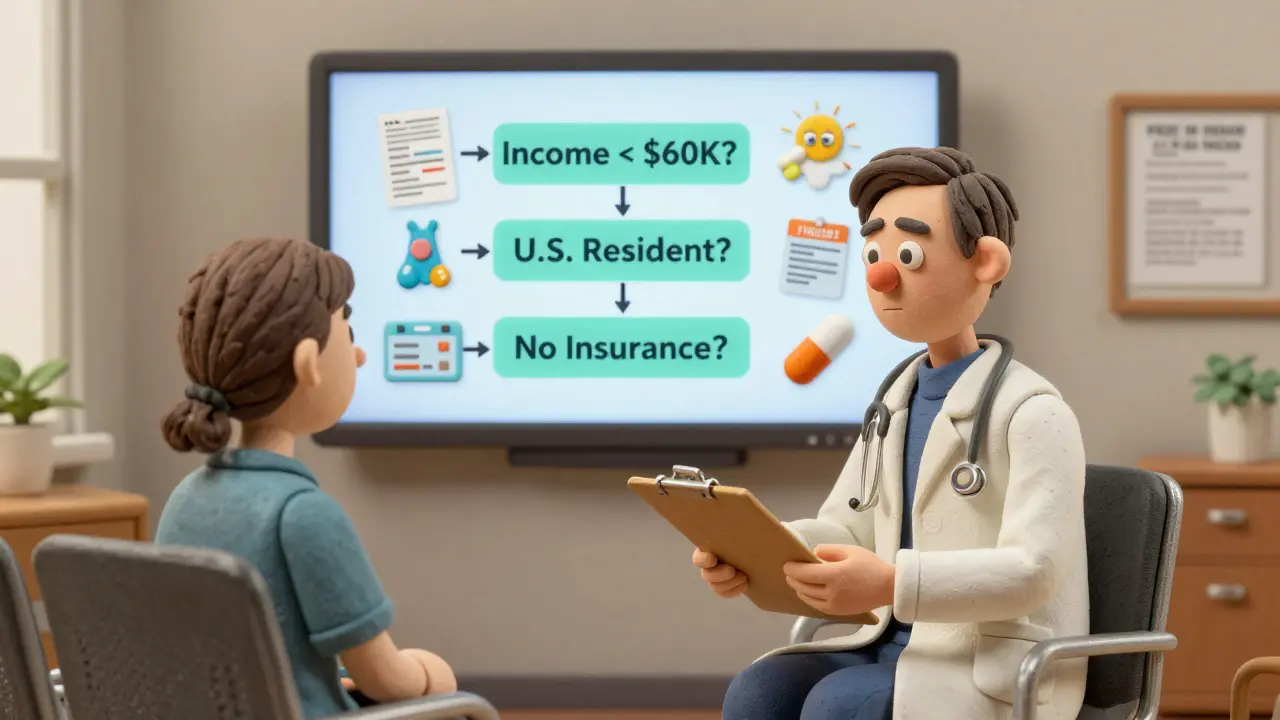

PAPs are stricter about income. Most require your household income to be under 400% of the Federal Poverty Level. For a family of four in 2023, that’s about $60,000 a year. You’ll need to prove it with tax returns, pay stubs, or a letter from a social services agency. You also need to be a U.S. resident. Some programs require you to have no other prescription coverage at all. That means if you have even Medicaid, you might be turned away-even if it doesn’t cover your specific drug.

What You’ll Pay: Real Numbers

The savings can be huge-if you qualify.With a copay card, you might pay as little as $10 to $15 per prescription. For example, Asthma and Allergy Foundation of America reports that patients on Dulera (a combination inhaler) can pay $15 per prescription with a manufacturer coupon, saving up to $90 per fill. Annual limits vary: some cards cap at $1,000, others at $25,000. Monthly caps are common too-often $50 to $200 per month. Some programs require you to pay a small fee each time, like $10, just to keep using the card.

With PAPs, you might pay nothing at all. Teva’s Cares Patient Assistance Program, for instance, provides certain generic and brand-name medications at no cost to eligible U.S. residents. Insulin programs from manufacturers like Eli Lilly and Novo Nordisk offer $35 monthly caps for people who qualify. But here’s the catch: PAPs don’t count toward your Medicare Part D out-of-pocket spending. That means if you’re on Medicare and rely on a PAP for your expensive drug, you won’t move closer to catastrophic coverage. You could stay stuck in the coverage gap longer.

How to Apply: The Process Is Messy, But It’s Doable

Applying for help isn’t simple. It’s not like signing up for a streaming service.For copay cards, it’s usually fast. You go to the drug maker’s website, enter your info, print or download the card, and bring it to the pharmacy. Some programs even let your doctor’s office apply for you. The whole thing can take 10 minutes.

PAPs? That’s a different story. You need to fill out a long form, get your doctor to sign off on medical necessity, and send in proof of income. The average application takes 45 to 60 minutes. Some require annual re-enrollment. Others give you coverage as long as you stay eligible. The Medicine Assistance Tool (MAT), run by the pharmaceutical industry group PhRMA, is the best starting point. It’s free, confidential, and lets you search over 900 programs by drug name, income, or insurance status. You don’t have to be tech-savvy to use it.

Why These Programs Exist-and Why They’re Controversial

Supporters say these programs save lives. Dr. Jane Smith from the Brookings Institution estimates that without copay assistance, 2.3 million more Americans would skip doses or stop taking their meds because they can’t afford them. For people with chronic conditions like diabetes or multiple sclerosis, that’s not just inconvenient-it’s dangerous.But critics have real concerns. A 2022 study in JAMA Internal Medicine found that copay assistance programs push patients toward more expensive brand-name drugs-even when cheaper generics are available. That drives up total drug spending by an estimated $1.4 billion a year. It also rewards companies for pricing drugs sky-high, knowing they’ll just cover the difference later.

And there’s a deeper issue: these programs are a patch, not a solution. They don’t fix broken drug pricing. They just help people survive it. As the National Institutes of Health pointed out in 2021, no one is tracking how many people actually use PAPs, or whether they’re helping the right people. And with 28 million Americans still uninsured, these programs are filling a gap the system should have closed.

What’s Changing in 2026?

The landscape is shifting fast. As of January 2024, 22 states have passed laws to regulate or ban copay cards for Medicaid patients. California now requires drug makers to publicly report how much they spend on these programs. The federal government is also looking at new rules to increase transparency.At the same time, tech is making access easier. PhRMA’s MAT platform now connects directly with pharmacy systems, so your discount can be applied automatically at checkout. Some manufacturers are even offering text-based eligibility checks so you don’t have to fill out a 10-page form.

But the big question remains: will these programs keep growing? Analysts at Evaluate Pharma predict the market will hit $38.2 billion by 2027. That’s up from $24.5 billion in 2022. More people will need them. But without real reform, we’re just moving money around-instead of lowering prices.

What You Should Do Right Now

If you’re struggling to pay for your meds:- Check the Medicine Assistance Tool (MAT) at www.medicationassistancetool.org. It’s free and confidential.

- Ask your pharmacist: "Does this drug have a manufacturer copay card?" They often have them on hand.

- If you’re uninsured or underinsured, ask your doctor’s office for help applying for a PAP. Many have patient advocates who do this daily.

- Don’t assume you don’t qualify. Income limits vary. Some programs accept people earning up to $75,000 a year.

- Keep your documents ready: tax returns, pay stubs, ID, insurance card, and a list of your prescriptions.

These programs aren’t perfect. But they’re real. And for millions of people, they’re the difference between health and hardship.

Can I use a manufacturer copay card if I’m on Medicare?

No, you generally cannot use manufacturer copay cards if you’re enrolled in Medicare Part D. Federal rules prohibit these cards from being used to reduce costs for Medicare beneficiaries. Some insurers also have "copay accumulator" programs that block the discount from counting toward your deductible, even if you try to use it. However, you may still qualify for a Patient Assistance Program (PAP) if your income is low enough.

Do PAPs cover all medications?

No. PAPs only cover specific brand-name drugs offered by the manufacturer running the program. Generic medications usually aren’t included. Also, not every drug from a company has an assistance program-especially older or less expensive ones. Always check the manufacturer’s website or use the Medicine Assistance Tool to see if your exact drug is covered.

Can I apply for more than one PAP at a time?

Yes. If you take multiple medications from different manufacturers, you can apply for assistance with each one. Many people use several PAPs at once to cover all their prescriptions. Just be prepared for separate applications, documentation, and renewal dates for each program.

Why don’t PAPs count toward Medicare’s out-of-pocket limit?

Medicare rules require that PAP assistance be kept separate from the Part D benefit. This means the value of free drugs from a PAP doesn’t count as your own spending, even though you’re getting the medication. This was designed to prevent drug makers from artificially lowering your out-of-pocket costs to help you reach catastrophic coverage faster. But it can leave you stuck in the coverage gap longer.

What if I make too much for a PAP but still can’t afford my drug?

You might still qualify for a copay assistance card if you have private insurance. If you’re uninsured and earn too much for a PAP, look into nonprofit organizations like the Patient Advocate Foundation or NeedyMeds. Some states also have their own prescription assistance programs. And always ask your doctor-they may have samples or know of local resources.

Are these programs only for U.S. residents?

Yes. All major manufacturer assistance programs in the U.S. require you to be a legal U.S. resident. They are not available to people living outside the country, even if they’re U.S. citizens. If you live in Australia or another country, you’ll need to explore local government or nonprofit options for drug affordability.

Uche Okoro

January 25, 2026 AT 11:12Let’s be clear: copay assistance programs are a regulatory arbitrage mechanism disguised as altruism. The pharma industry leverages Section 1108 of the Social Security Act to circumvent anti-kickback statutes while simultaneously inflating list prices-then subsidizes the very distortions they engineered. It’s a classic case of market failure externalized onto patients. The $24.5B in PAP disbursements? That’s not charity-it’s a cost-shifting maneuver to preserve premium pricing power under the guise of patient advocacy. The system isn’t broken; it’s optimized for shareholder returns, not health equity.

Ashley Porter

January 27, 2026 AT 06:23Honestly, I didn’t even know PAPs existed until my mom got diagnosed with RA. We applied for hers through MAT and got her biologic for free. Took 3 weeks, paperwork was brutal, but worth it. I just wish more people knew this was an option. It’s not magic, but it’s real help when you’re drowning in bills.

shivam utkresth

January 29, 2026 AT 02:56Man, this hits different when you’re from a country where insulin costs 10x more than here and you still can’t get it without begging. I’m from India, and we’ve got our own mess-private pharma hoarding generics, no safety nets. But seeing U.S. programs like this? It’s a glimpse of what’s possible. Even if it’s patchwork, it’s better than nothing. Kudos to MAT for making it less of a labyrinth. Maybe one day global access won’t be a joke.

Kipper Pickens

January 29, 2026 AT 16:12Interesting breakdown, but let’s not romanticize this. These programs are corporate PR with clinical outcomes. The fact that 85% of specialty drugs offer copay cards? That’s not generosity-it’s a pricing strategy calibrated to maximize revenue while avoiding political backlash. And don’t get me started on the Medicare Part D loophole. It’s a deliberate design flaw that keeps seniors in the doughnut hole. The system isn’t broken-it’s engineered this way.

Aurelie L.

January 31, 2026 AT 05:18So basically, if you’re rich enough to have insurance but poor enough to need help, you’re stuck in a bureaucratic purgatory. And if you’re on Medicare? Too bad. You’re just supposed to suffer quietly. This isn’t healthcare. It’s a horror show with a corporate logo.

Joanna Domżalska

January 31, 2026 AT 16:27Wow. So we’re celebrating corporations giving back some of the money they stole from us? That’s your solution? Instead of forcing them to lower prices, we just hand out coupons? This is like giving a starving person a napkin to wipe their tears. Pathetic.

Sally Dalton

February 2, 2026 AT 09:09OMG I JUST FOUND OUT MY DRUG HAS A CO-PAY CARD AND I’VE BEEN PAYING $180 A MONTH?? I’M CRYING RN. I’M SO SORRY I DIDN’T KNOW THIS EXISTED. I THOUGHT I WAS JUST BAD AT BUDGETING. THANK YOU FOR THIS POST!! I’M GOING TO APPLY RIGHT NOW!!

Shawn Raja

February 4, 2026 AT 06:21Look, I get it. These programs save lives. But they’re also a Band-Aid on a hemorrhage. Pharma companies set the price at $10,000/month, then give you $9,900 off. That’s not help-that’s theater. And the fact that they get tax breaks for it? That’s just salt in the wound. Meanwhile, my cousin in Canada pays $5 for the same drug. We’re not broken-we’re being looted.

Ryan W

February 4, 2026 AT 23:48Another one of these feel-good corporate PR pieces. Let’s not forget: these companies lobby against price caps, then hand out coupons to keep you quiet. And now we’re supposed to be grateful? If you’re a U.S. citizen, you’re paying for this mess through taxes, premiums, and inflation. Stop patting yourself on the back. This isn’t compassion-it’s control.

TONY ADAMS

February 6, 2026 AT 17:07Bro I just got my insulin for $35 a month. No joke. I was gonna cut my dose in half. Now I’m not. Just go to the website. It’s not hard. You don’t need a degree. Just do it.