Every year, millions of Americans face unexpected medical bills that crush their finances. Some get hit with surprise charges after emergency care. Others are pressured into signing up for medical financing they don’t understand. And too many find medical debt showing up on their credit reports-making it harder to rent an apartment, buy a car, or even get a job. In 2024, New York State stepped in with some of the strongest patient protection laws in the country. These aren’t just paperwork changes. They’re real rules that stop hospitals and clinics from taking advantage of people when they’re most vulnerable.

Separate Consent for Treatment and Payment

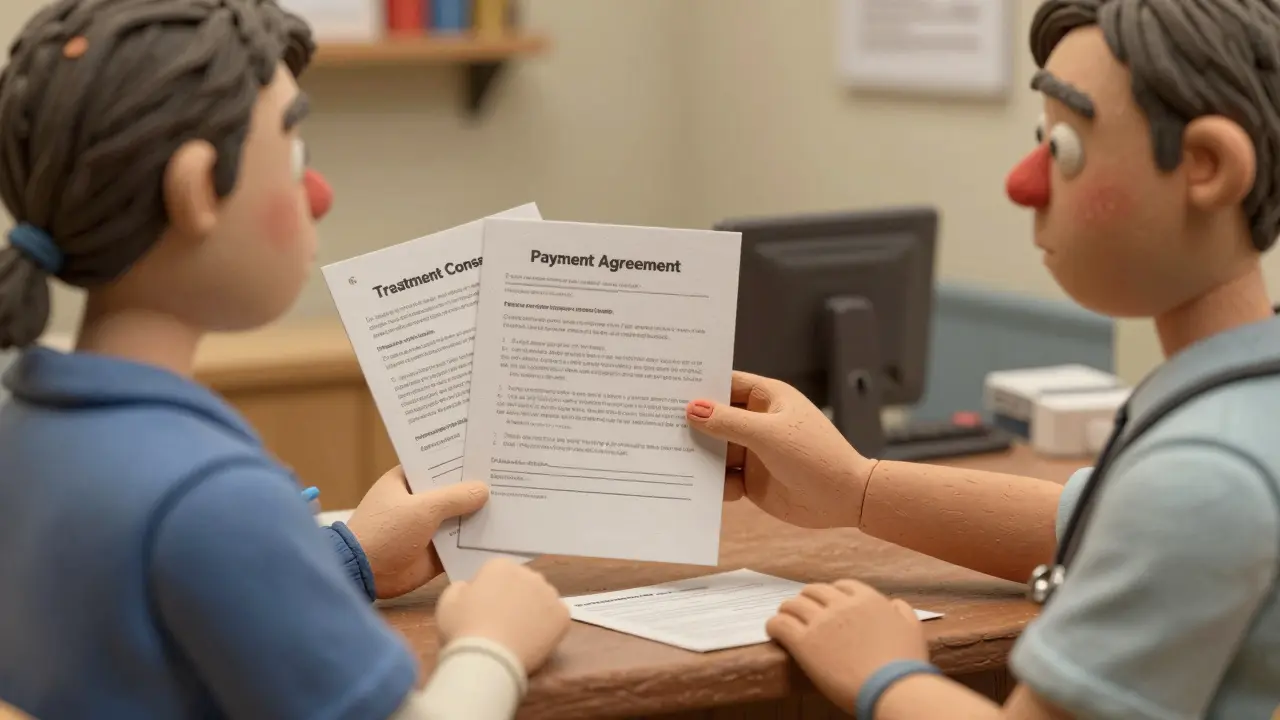

For years, patients walked into clinics and signed one form that did two things: it gave consent for treatment and agreed to pay for it. That form was often long, full of legal jargon, and signed without reading. Many patients didn’t realize they were also agreeing to financial terms-like allowing the provider to use their credit card on file or enroll them in a medical financing plan. Starting October 20, 2024, New York law changed that. Public Health Law Section 18-c now requires providers to get two separate signatures: one for medical care and another for payment. You can’t sign one form and think you’ve covered everything. If a provider asks you to sign a single document that combines both, you have the right to refuse-and they can be fined $2,000 per violation. This law targets a common trick: using intake forms to sneak in financial agreements. It doesn’t mean you can’t pay for care. It means you have to make that decision on your own, clearly and without pressure. You should never feel rushed into signing anything when you’re in pain, stressed, or confused.Doctors Can’t Fill Out Your Medical Financing Applications

Have you ever been told, “We’ll help you apply for CareCredit”? That’s no longer allowed under New York’s General Business Law Section 349-g. Providers can answer your questions about financing options. They can hand you the application. They can even tell you what documents you’ll need. But they cannot touch the form. Not one box. Not one signature. Not even filling in your name. Why? Because medical financing companies like CareCredit, LendingClub Medical, or CareOne often charge high interest rates. Some have deferred interest clauses-if you don’t pay off the balance in 12 months, you owe all the interest retroactively. Providers used to push these products because they got paid faster. You ended up paying more, and sometimes got stuck with debt you didn’t fully understand. Now, the law puts the power back in your hands. If you want to apply for medical financing, you do it yourself. No staff member can guide you through the form. No one can pre-fill your information. If they do, they risk a $5,000 fine per violation.No More Credit Cards on File Before Emergency Care

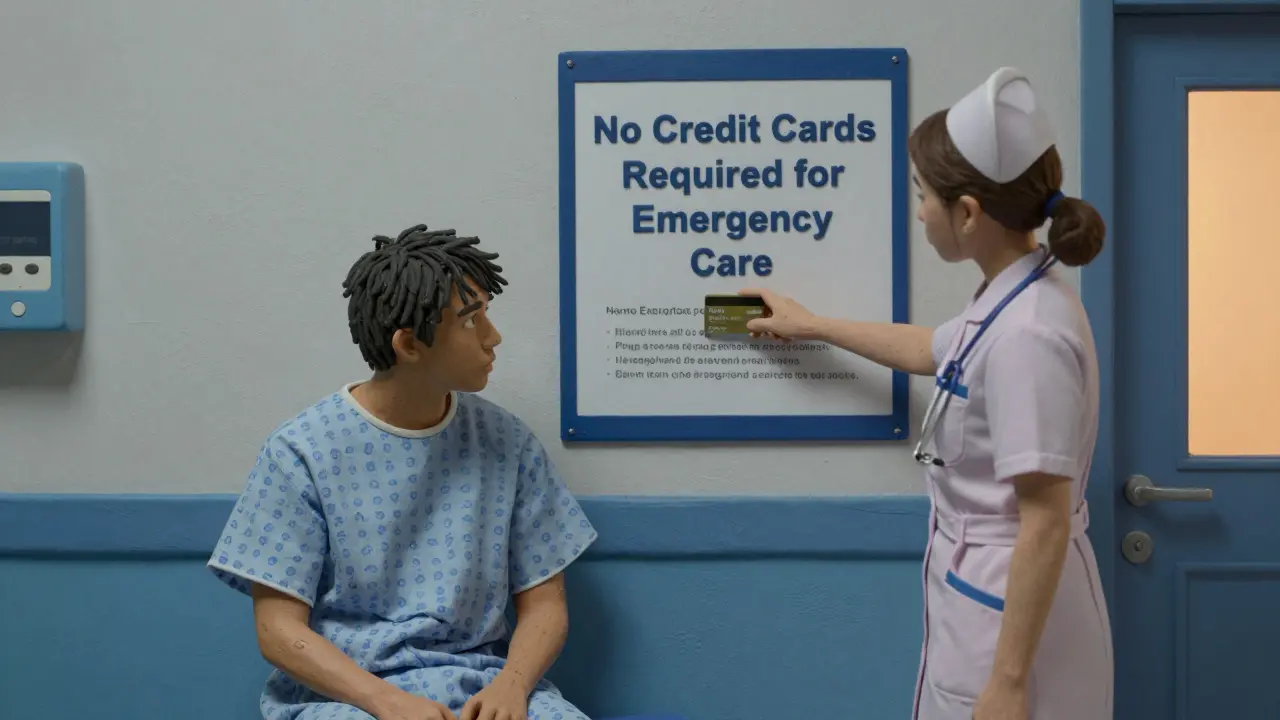

Imagine you’re rushed to the ER after a fall. You’re in pain. Your head is spinning. The front desk asks for your credit card. “We need to keep it on file,” they say. That’s illegal now under General Business Law Section 519-a. Providers can’t require you to give them your credit card before giving you emergency or medically necessary care. They can’t hold it on file. They can’t ask for a preauthorization. They can’t even say, “We’ll just run it if needed.” This law closes a dangerous loophole. If you pay with a regular credit card, you lose access to federal and state protections. Medical debt from CareCredit or other healthcare-specific financing programs can’t be reported to credit bureaus, can’t lead to wage garnishment, and can’t result in liens on your home. But if you pay with a Visa or Mastercard? All those protections vanish. You’re treated like any other consumer debt-and that’s exactly what the law was designed to stop.

What About the No Surprises Act?

You might have heard about the federal No Surprises Act, which started in January 2022. That law protects you from surprise bills when you get care from an out-of-network provider-like an anesthesiologist at an in-network hospital. It doesn’t cover everything, though. It doesn’t stop providers from asking for your credit card on file. It doesn’t require separate consent forms. It doesn’t stop them from pushing medical financing. New York’s laws go further. They target the everyday financial traps that happen even when you’re seeing in-network doctors. The federal law stops surprise charges. New York stops surprise debt.What Happens If You Pay With a Regular Credit Card?

This is critical: if you use a regular credit card to pay your medical bill, you’re not protected by the same rules as medical financing. Medical debt from CareCredit or similar programs can’t be sent to collections without notice. It can’t be reported to credit bureaus. It can’t lead to wage garnishment or property liens. But if you use your personal credit card? All those protections disappear. That debt becomes just like any other-credit card debt. And that means it can hurt your credit score, lead to collection calls, and even be sold to debt buyers. New York law now requires providers to tell you this every time you use a credit card. You should receive a written notice explaining the risks. If you don’t get it, ask for it. If they refuse, you can file a complaint with the New York State Department of Health.What About the Suspension of Section 18-c?

There’s confusion. In August 2025, some legal advisors reported that Public Health Law Section 18-c-the rule requiring separate consent forms-had been suspended. That’s true. But it’s not gone. It’s on hold while officials review implementation issues. The other two laws (about medical financing and credit cards) are still fully in effect. If you’re a patient, this doesn’t change your rights. The intent of the law is still clear: you should know exactly what you’re signing. Even if the rule isn’t being enforced right now, providers are still expected to follow best practices. Don’t sign anything that combines treatment and payment. Ask for separate forms. If they push back, you’re still protected under the spirit of the law.

What You Can Do Right Now

You don’t need a lawyer to protect yourself. Here’s what to do before you sign anything:- Never sign one form for both treatment and payment. Ask for two separate documents.

- If someone offers to help you apply for CareCredit or another medical loan, say no. Fill it out yourself-or walk away.

- If you’re asked for a credit card before emergency care, say no. You have the right to refuse.

- Always ask: “Is this payment covered under medical debt protections?” If they say yes, ask for proof. If they say no, know you’re on your own financially.

- Keep copies of every form you sign. If something goes wrong later, you’ll need proof.

Is This Happening Elsewhere?

New York isn’t alone. The Consumer Financial Protection Bureau (CFPB) banned medical debt from credit reports in 2024. That’s a huge win for patients nationwide. Other states are watching. California, Illinois, and Washington are already drafting similar bills. In 2026, you can expect more states to follow New York’s lead. This isn’t about making hospitals lose money. It’s about stopping predatory practices. Providers need to get paid. Patients need to be treated fairly. These laws make that possible.Final Thought: Know Your Rights

Medical care shouldn’t mean financial ruin. You’re not a credit risk when you’re sick. You’re a patient. And you deserve to be treated like one. These laws give you power. Use it. Ask questions. Say no when something feels off. Keep records. And if you’re unsure, contact your state’s health department. You’re not alone-and you’re not powerless.Can a hospital require my credit card before treating me in an emergency?

No. Under New York’s General Business Law Section 519-a, healthcare providers cannot require you to provide or keep a credit card on file before giving emergency or medically necessary care. This rule applies even if you’re insured. You have the right to receive treatment without being asked for payment details upfront.

What’s the difference between CareCredit and a regular credit card for medical bills?

CareCredit and similar medical financing programs are designed specifically for healthcare. They’re protected under New York’s medical debt laws: they can’t be reported to credit bureaus, can’t lead to wage garnishment, and can’t result in liens on your home. Regular credit cards offer none of these protections. If you pay a medical bill with a Visa or Mastercard, that debt becomes regular consumer debt-with all the risks that come with it.

Can my doctor fill out my medical financing application for me?

No. Under New York’s General Business Law Section 349-g, providers are forbidden from completing any part of a patient’s application for medical financing products like CareCredit. They can answer questions or hand you the form, but they cannot write anything on it-not even your name. If they do, it’s a violation punishable by up to $5,000 per incident.

Do I need to sign separate forms for treatment and payment?

Yes. New York’s Public Health Law Section 18-c requires healthcare providers to obtain separate, written consent for treatment and for payment. While enforcement of this section is currently suspended as of August 2025, the intent remains clear: patients should understand what they’re agreeing to. You should still ask for two separate forms. If a provider refuses, you have the right to walk away or file a complaint.

What should I do if I’m pressured to sign a medical financing agreement?

Pause. Ask for time to think. Don’t sign anything under pressure. If someone insists you need to sign now to get care, they’re violating the spirit-and possibly the letter-of the law. You can ask to speak with a patient advocate, request a copy of the form to review later, or simply say no. If you feel coerced, report the incident to the New York State Department of Health. You’re not obligated to make financial decisions while you’re in pain or stressed.

Vince Nairn

January 7, 2026 AT 23:41Good riddance to those 'one form to rule them all' scams.

Ayodeji Williams

January 8, 2026 AT 06:48Kyle King

January 9, 2026 AT 01:24Kamlesh Chauhan

January 10, 2026 AT 05:45Emma Addison Thomas

January 11, 2026 AT 00:11Mina Murray

January 11, 2026 AT 07:14Rachel Steward

January 12, 2026 AT 05:50And yes, I’ve seen patients sign away their future because they were too scared to say no. But this law doesn’t fix fear. It just adds a signature line.

Christine Joy Chicano

January 13, 2026 AT 22:39Still... I’m glad someone’s trying. I once signed a 12-page consent form after a sprained ankle. I didn’t realize until two months later that I’d agreed to a 24% APR loan. I cried in the pharmacy aisle. This law would’ve saved me that trauma.

Adam Gainski

January 15, 2026 AT 04:40Biggest issue? Patients still don’t read anything. We give them the forms in plain language, and they still sign without looking. So the law helps... but education matters more.

Anastasia Novak

January 15, 2026 AT 10:54Jonathan Larson

January 17, 2026 AT 08:18Alex Danner

January 17, 2026 AT 09:34And yes, the 'suspension' of Section 18-c? That’s a loophole they’re already exploiting. Hospitals are back to combining forms but calling it 'consolidated consent.' It’s the same scam, just rebranded. Keep copies. Always.

Jessie Ann Lambrecht

January 19, 2026 AT 07:02Elen Pihlap

January 20, 2026 AT 09:47Jonathan Larson

January 21, 2026 AT 20:35